A bank or financial institution thoroughly checks each application before approving a loan. It

Reduces the risk of default and helps in knowing the repayment capability of a borrower. The CAM reports give all the overall details of the borrower. It helps banks to make the right lending decision and reduce NPAs.

What is the full form of CAM in Banking?

The full form of CAM in banking is Credit Appraisal Memorandum and Credit Analysis Memorandum. The credit officer prepares this report. It helps in checking the creditworthiness of the borrower. It helps in rejecting or modifying the loan request.

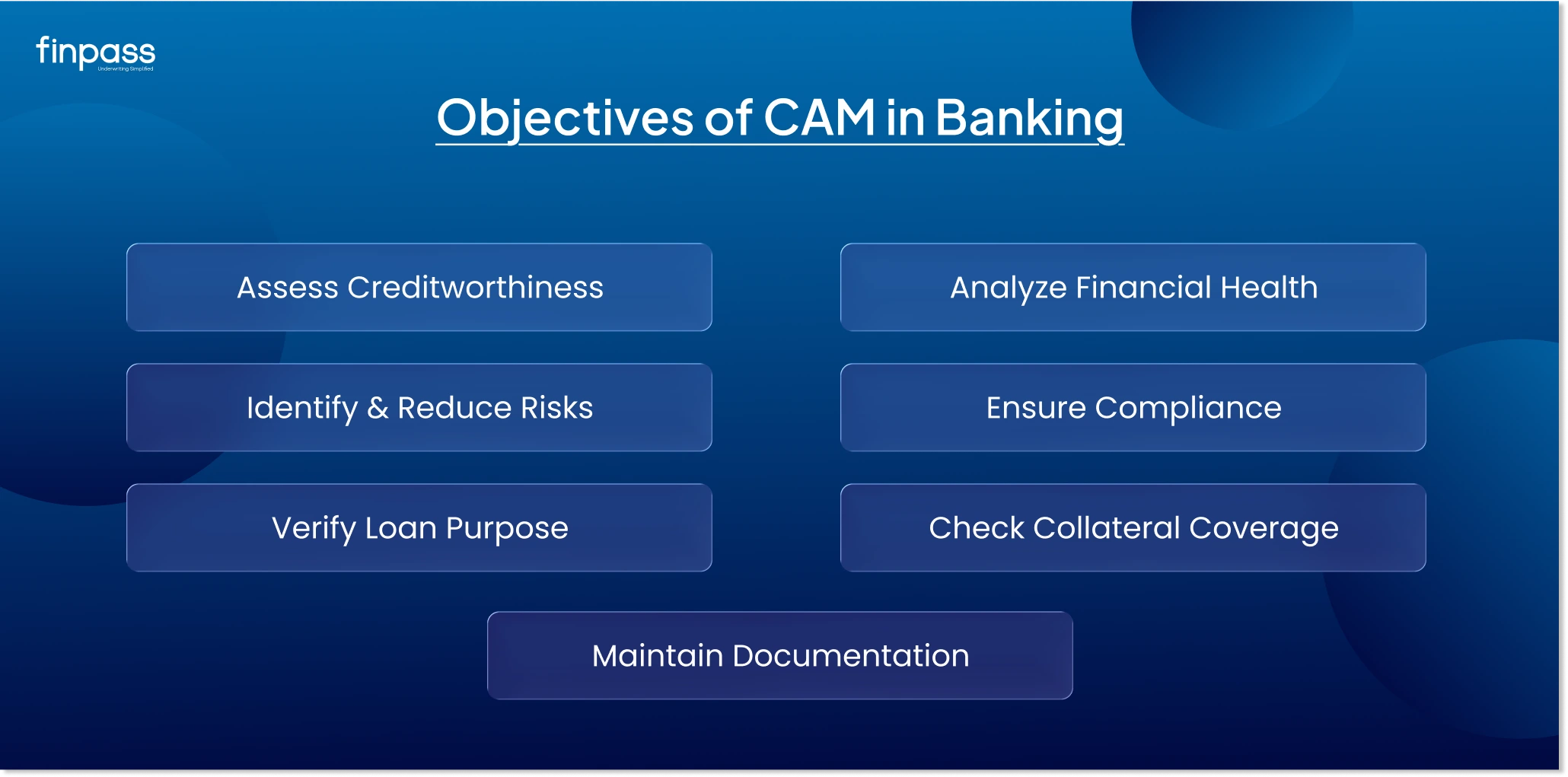

Objective of CAM

It is used for the following reasons:

- Assess Borrower’s Creditworthiness: It helps banks evaluate whether the borrower can repay the loan based on financial history and current location.

- Analyse Financial Health: It provides a detailed analysis of financial statements such as balance sheets, profit and loss accounts, and cash flows to understand the business’s stability.

- Identify and Reduce Risks: This report highlights potential risk factors, including financial, operational, or market-related. So that banks can take proper precautions before loan.

- Compliance: It confirms that the loan proposal follows internal policies, regulatory guidelines, and risk management frameworks.

- Evaluate Purpose and Utilization of the Loan: It verifies whether a loan is being taken for a valid and productive purpose, including business expansion or working capital.

- Security and Collateral Coverage: It checks whether the asset (like property, gold, or other valuables) are enough to cover the loan amount.

- Maintain Documentation: It creates a structured record of the entire credit evaluation process.

What Documents are Required to Prepare a CAM Report?

These are the following documents used to prepare a CAM Report:

- KYC Documents

- Bank Statements

- Income Tax Returns (ITR)

- Financial Statements

- Credit Reports (like CIBIL)

Key Components of CAM

These are the main components of the Credit Analysis Memorandum:

- Borrower Information: It covers basic details of the customer, including business type, ownership structure, KYC documents, banking relationship, and past payment records.

- Business Overview: Information about the company's operations, industry, products/services, and market positions.

- Financial Analysis: It contains a review of financial statements (balance sheet, profit and loss, cash flow) to check performance and stability.

- Loan Details: Purpose of the loan, amount required, type of loan, and repayment plan.

- Credit History: It also includes past borrowing record, repayment behaviour, and the credit score of the borrower.

- Collateral and Security: It contains details of assets provided by the borrower against the loan.

- Risk Assessment: Identification of possible risks (business risk, financial risk) involved in lending.

- Compliance Check: It confirms that the loan proposal follows bank policies and regulatory guidelines.

Importance of CAM Report in Banking

There are many benefits of using the CAM report in banking:

- It helps reduce the risk of bad loans (NPAs) by analyzing the borrower's credibility in detail.

- It allows banks to make well-informed and data-driven lending decisions.

- It strengthens the bank’s financial stability by minimising potential losses.

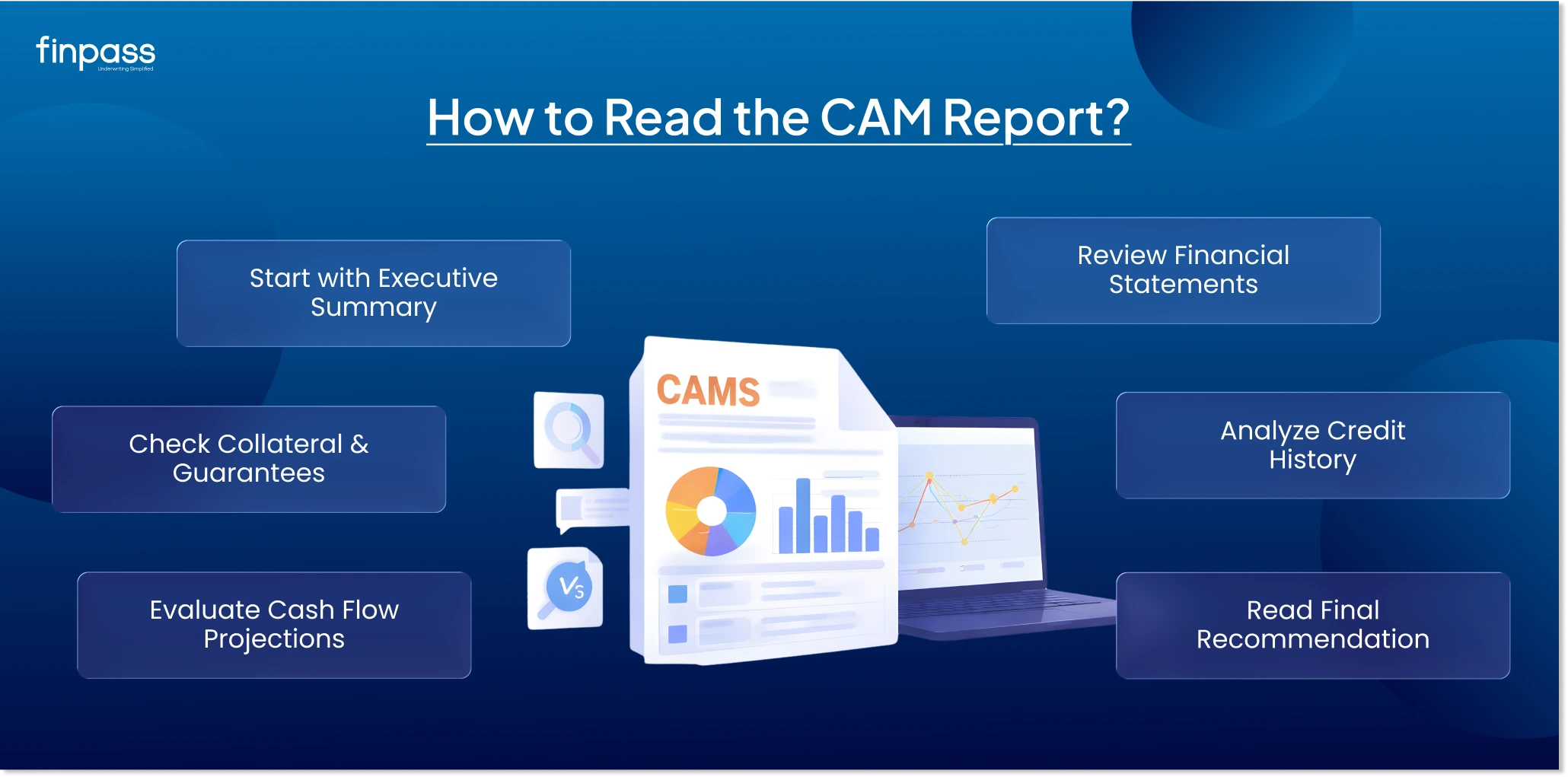

How to Read the CAM Report?

The CAM report looks difficult to understand. You can follow the steps below to read the CAM Report:

- State with the Executive Summary: First, start with the executive summary, it gives an overview of the borrower’s financial condition and overall risk.

- Check the Financial Statements: Check the balance sheet, profit and loss statement, and cash flow statement. It helps you check profit and overall financial stability.

- Look at Collateral and Guarantees: You will find information about assets given as security and any guarantees from the borrower or third parties. It helps lenders feel that the borrower or third parties.

- Review the Borrower’s Credit History: This section shows the borrower’s past loan behaviour, including repayment and defaults. It helps judge how reliable the borrower is.

- Check Cash Flow Projection: This part shows future income and expenses. It helps the lender see if the borrower will have enough money to repay the loan on time.

- Read the Final Recommendation: This is the last part of the CAM report that approves the loan, rejects the loan, or suggests changes in terms.

How Finpass Simplifies CAM Preparation?

We have already understood the value of the CAM report in lending. However, manually preparing this report is time-consuming. Finpass is an underwriting solution.

It uses advanced financial analysis and helps banks, NBFCs, and financial institutions automate and streamline the CAM preparation process. It collects, verifies, and analyzes borrower data efficiently.

Wrap Up

A CAM report is an essential part of banking. It helps in checking the borrower’s financial repayment capability. The above guide helps you understand CAM in detail. Manually preparing CAM is difficult automated solution like Finpass helps businesses streamline the Credit Appraisal Memorandum preparation work.

FAQs

Ques: What is the full form of CAM in Banking?

Ans: Credit Appraisal Memorandum and Credit Analysis Memorandum.

Ques: Who uses CAM in banking?

Ans: Credit Analystics and underwriters use this report for checking borrowers' financial credibility.

Ques: What are the types of CAM in Banking?

Ans: It is classified into:

- Retail CAM (for individuals)

- Corporate CAM (for Business)

- MSME CAM (for small businesses and medium enterprises)

Ques: Is CAM used for all types of loans?

Ans: Yes, it is used for Personal Loans, Home Loans, Business Loans, and MSME and Corporate Financing.

Ques: What are red flags in a CAM report?

Ans: Common red flags include:

- Irregular Cash Flow.

- High Debt Levels.

- Poor Credit History.

- Inconsistent Financial Statements.