UPI payments no longer depend on your bank balance alone; earlier payments would simply fail if they did not contain enough funds, leaving you stuck at checkout. Now with pre-approved credit lines directly linked to your UPI ID, this problem has been eliminated - whether online shopping or at a physical store, or paying utility bills, you can complete payments even when your balance is low or empty without needing extra apps, paperwork or waiting - instant credit available when needed!

What is a Credit Line?

A credit line is a pre-approved amount of money that a bank or lender allows you to borrow when needed. You can use any portion of it and pay interest only on what you use, not the full limit. As you repay the borrowed amount, your available credit is restored. It works like a flexible loan and is commonly used through credit cards or credit lines on UPI.

Credit Line on UPI Meaning

UPI credit lines are digital credit limits provided by your bank in the form of Rupay credit cards that can be linked directly to your UPI ID just like a savings account. Instead of withdrawing money directly from savings accounts, the UPI app pulls money from this credit line, allowing you to borrow funds for daily transactions which need to be repaid as per a repayment schedule.

How Credit Line on UPI Works

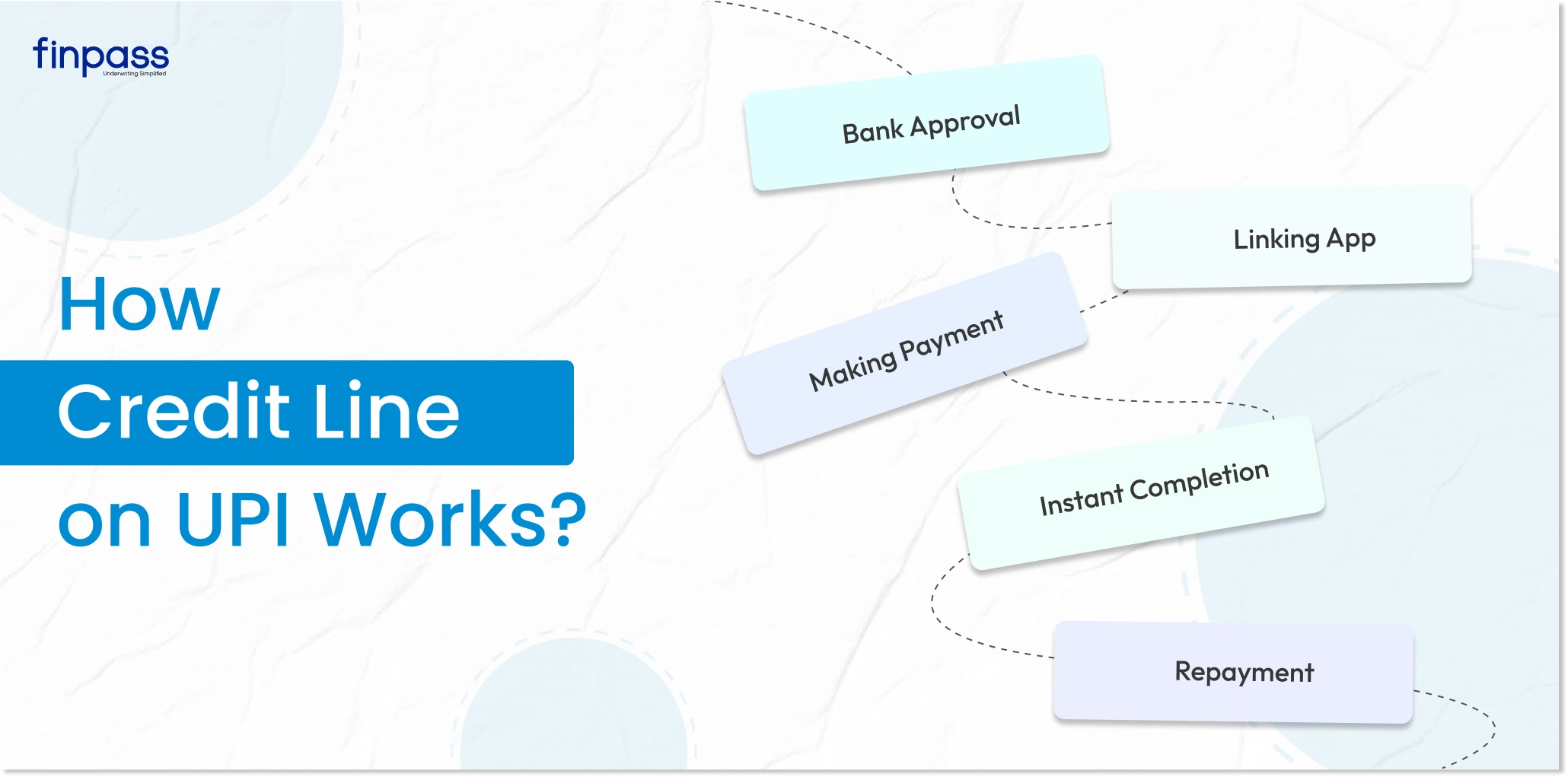

Credit on UPI has been designed to be entirely digital and paperless, as shown below in a step-by-step flow of how the system currently functions:

- Bank Approval: Your bank evaluates your financial profile, such as income and spending habits. If approved, they set a specific credit limit for you such as Rs10,000 or Rs 50,000.

- Linking App: Once you open one of your UPI apps such as Google Pay, PhonePe, or BHIM, navigate to your profile and add a new payment method as Rupay Credit Card.

- Making Payment: At stores or online checkouts, simply scan QR code or enter the merchant’s UPI ID to make the payment. When selecting which UPI-ID to pay with - select the one ending with the last-4 digits of your Rupay credit card and continue to make the payment as usual.

- Instant Completion: Payments are done instantly and securely over UPI network and merchants receive their funds instantly without affecting your bank balance.

- Repayment: At the end of your billing cycle or by its due date, your borrowed amount must be repaid to the bank via a cheque or online payment using apps like PhonePe and Google Pay.

Key Features of UPI Credit Line

- Pre-approved Credit: No need to wait in line at the store, because your limit has already been determined based on your transaction history and credit score.

- No Bank Balance Needed: One of the main advantages is user does not need a bank balance to make urgent payments if their salary or savings account is still short of funds.

- Standard QRs: No special QR code is necessary as UPI payments work on all merchant QR codes that accept it.

- Digital Online Payments: Digital Online Payments extend beyond physical shops to include online shopping, food delivery apps, and ticket booking.

- Integral System: No new apps need to be downloaded - your credit line will be directly tied into the UPI apps you already use every day.

- Flexible Repayment Solutions: Depending on the bank you use, flexible repayment options may allow you to either make full payments at once or divide larger purchases into monthly payments.

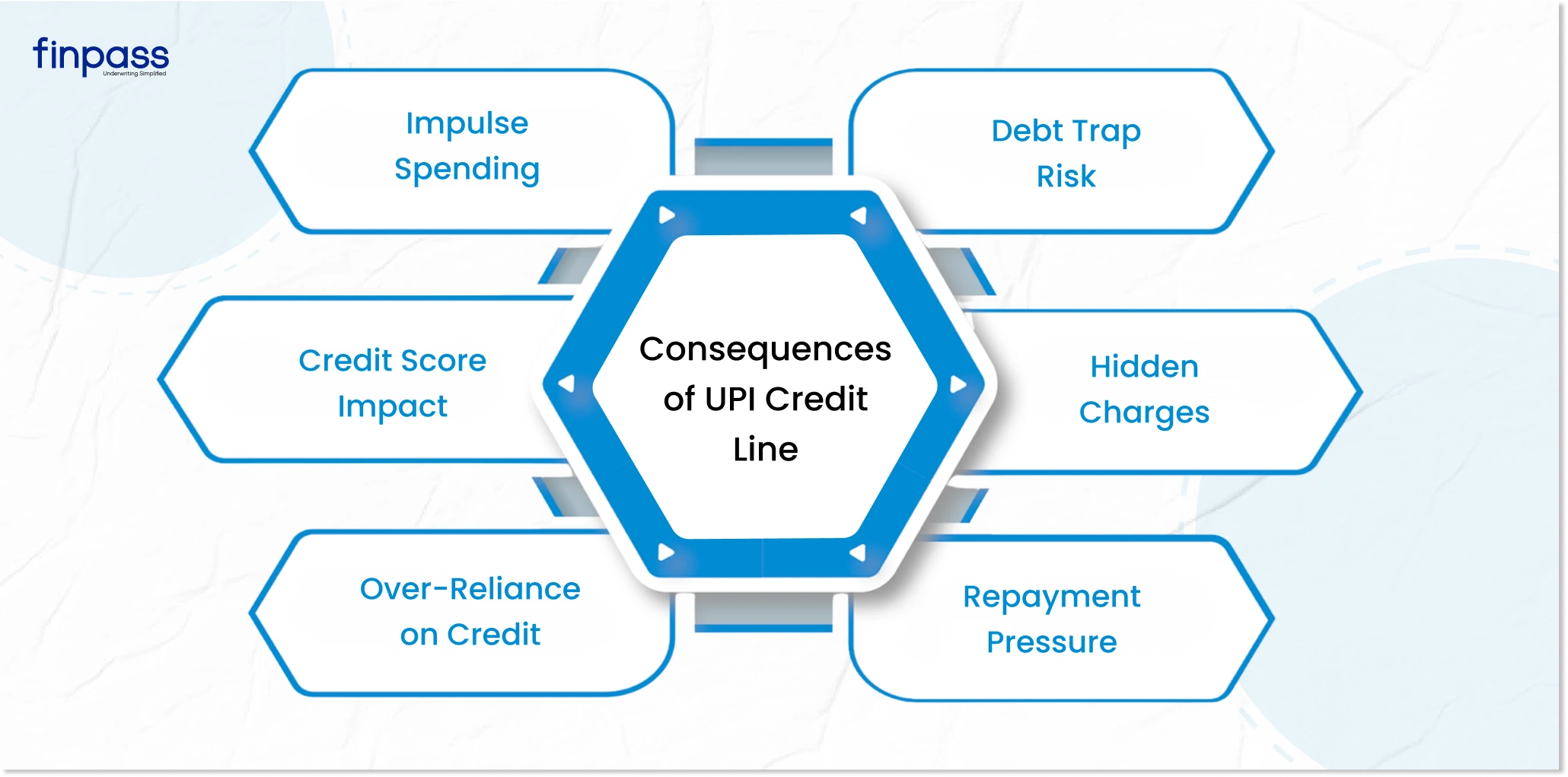

Consequences of the UPI Credit Card

While UPI Credit Line is an excellent tool, it comes with its own set of consequences. Such as:

- Impulse Purchases: UPI removes the pain of making a payment such as handing over cash or swiping a credit card, and makes it feel like just a QR scan for each purchase, many of which could have been avoided. With a credit line on UPI this becomes an even bigger issue as it makes you pay for things you might need and starts a circle of unnecessary borrowing.

- Debt Trap: Just like credit cards, UPI credit line comes with high interest rates and since it is highly accessible, the credit line gets used frequently and excessively to the point where you might not even be able to pay the sum back.

- Decrease in Credit Score: Credit score is highly sensitive that frequently changes every month depending on how you use your credit, and if you fail repayment of a UPI credit card your credit score may take a severe hit resulting in higher interest rates and charges by the banks for any financial help in the future.

- Hidden Charges: While UPI is typically free, linking a credit card can introduce fees such as transaction or convenience charges. These added costs can make everyday purchases more expensive than users expect.

How UPI Credit Line different from a credit card?

While both allow you to spend borrowed money, they have key differences:

- Physical vs Digital: Credit cards are physical pieces of plastic you carry around in your wallet; UPI credit lines exist solely online and stay inside your phone.

- Acceptance: Small shops in India may lack credit card machines due to cost concerns; however, almost every small shop does feature a UPI QR code, making credit lines more widely accepted by local markets.

- Fees: Credit cards often incur annual maintenance fees, while UPI credit lines have lower entry barriers or alternative fee structures depending on the bank offering them.

- Security: With several security measures like UPI PIN, biometric lock, and end-to-end encryption on transactions, there is no worry of losing or having your credit card stolen.

Where You Can Use UPI Credit Line

You can use a credit line on UPI for most merchant payments. This includes:

- Scanning QR codes at local grocery stores or pharmacies.

- Paying at petrol pumps.

- Online checkouts on e-commerce websites like Amazon or Flipkart.

- Paying utility bills like electricity or water.

Things to Keep in Mind

- Interest Rates and Fees: Borrowing money is rarely free. Banks may charge interest on the amount used or a one-time processing fee. Always read the fine print.

- Bank Eligibility: Not every customer will see this option. It depends on your relationship with the bank, your account balance history, and your credit score.

- Impact of Late Payments: Since this is a formal credit product, your usage is reported to credit bureaus like CIBIL. If you miss a payment, it will hurt your credit score.

- App and Bank Support: This feature is part of a phased rollout by the NPCI. Not all banks or UPI apps support it yet, though the number is growing every month.

Conclusion

Credit Line on UPI is a game-changer in Indian digital payments, making it possible to make transactions even when your bank balance runs low. Combining UPI's widespread reach with instant credit without needing extra apps or physical cards. But remember: responsible use is the key, timely repayments and awareness of interest rates will ensure that credit on UPI works in your favour! As adoption increases across banks and UPI platforms, Credit Line on UPI will soon become part of how India pays.

FAQs

Ques: What Is A Credit Line On UPI?

Ans: A credit line on UPI is a pre-approved borrowing limit provided by your bank that's tied directly to your UPI ID, enabling payments even when your bank balance is low or empty.

Ques: Which UPI Apps Support Credit Lines on UPI?

Ans: Popular apps like Google Pay, PhonePe and BHIM support UPI credit lines; availability depends on your bank and NPCI's ongoing rollout plan.

Ques: How can I link a credit line to my UPI app?

Ans: Open your UPI app, navigate to your profile, and open up the payment methods section - add your Rupay Credit Card as a payment method, and done you can use.

Ques: Is a credit line on UPI the same as a credit card?

Ans: No. While both allow you to borrow money, a UPI credit line differs in that it exists solely digitally with no physical card associated with it, accepted at all shops with UPI QR codes -- including smaller stores without card machines - for easy spending.

Ques: Do I require an excellent credit score to qualify for UPI on credit?

Ans: Yes. Your bank evaluates all aspects of your financial profile - credit score, income and transaction history - before approving the credit line on UPIl.

Ques: Is there any fee or Interest Charges?

Ans: Banks may charge fees and interest charges on amounts borrowed as well as one-time processing fees when using this feature, so it is wise to read their terms and conditions thoroughly prior to using this option.

Ques: What happens if I miss a repayment?

Ans: Missed repayments will be reported to credit bureaus such as CIBIL, potentially damaging your score and hindering future attempts at loan approval.