According to the reports, 53% of cash-related frauds are linked to weak internal controls, such as infrequent reconciliations. It highlights how effective bank reconciliation is important to prevent fraud. A bank reconciliation statement is not just an accounting formality. It helps fill the gap between internal financial records and external bank statements. It confirms that each transaction is accounted for.

What is a Bank Reconciliation Statement?

In simple words, A Bank Reconciliation Statement is a financial document that helps compare a company's account records with the bank statement. It helps in detecting discrepancies from transactions such as outstanding checks or deposits in transit. This statement is essential for financial reporting, internal controls, and fraud detection.

Purpose of Bank Reconciliation Statement

The main purpose of a bank reconciliation statement includes:

Match Bank Records with Accounting Records

It is used to match the Cash Book with the Bank Statement and check whether both of them match. It helps in matching the records if there is any difference seen in timing or adjustments.

Detects Errors - Both Bank and Bookkeeping Mistakes

Errors can occur in the bank system or your own accounting records. Examples include:

- Wrong Transaction Amounts

- Duplicate Entries

- Missed Deposits

- Incorrect Postings

Here, the Bank Reconciliation Statement helps identify the discrepancies and helps correct them.

Identify Fraud or Unauthorized Transactions

Unauthorized withdrawals, altered checks, or fake transactions can cause a difference between the bank and the book.

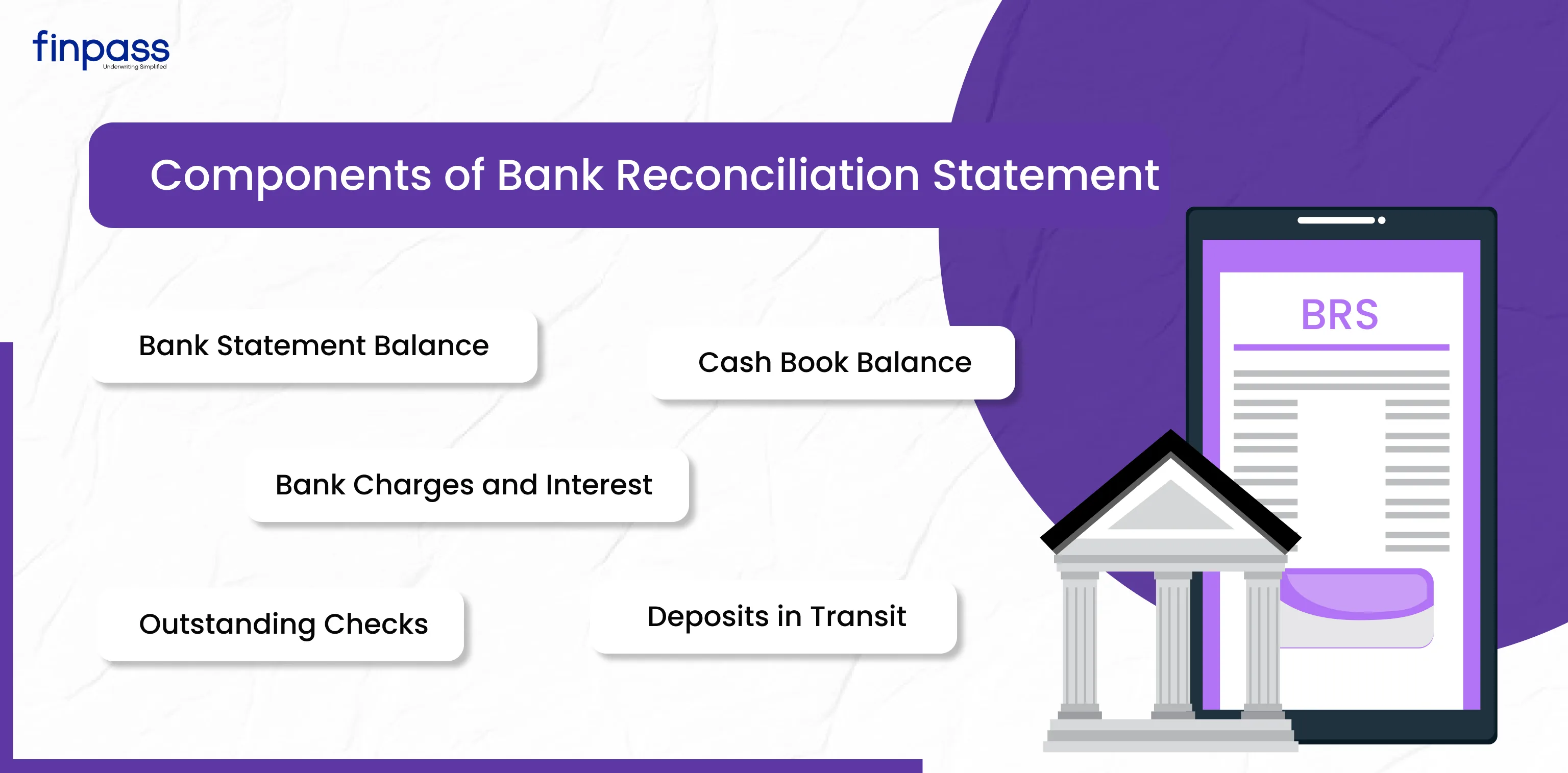

Main Components of Bank Reconciliation Statement

These are the key components of bank reconciliation statements that you must know;

- Bank Statement Balance

This is the closing balance shown on your bank statement for the specific period you are reconciling. It helps track all transactions the bank has processed, including cleared checks, deposited amounts, direct debits, and bank charges. This balance is different from the Cash Book because some transactions have not yet been recorded or cleared.

- Cash Book Balance

The Cash Book shows the business's internal record of cash and bank transactions. This balance includes payments issued, deposits made, and adjustment records.

- Deposits in Transit

It is also known as uncredited deposits. It refers to the recorded amount in your Cash Book, but the bank has not yet processed it. It typically occurs when deposits are made near the end of the day or at the end of the month.

- Outstanding Checks

When a business issues checks, it records them in the cash book, but does not present them to the bank. As the bank has not deducted these amounts yet, they must be subtracted from the bank statement balance during reconciliation.

- Bank Charges and Interest

Banks often deduct charges or credit interest directly to the account. It may not be recorded in your Cash Book. You must update the Cash book for all charges and interest entries for reconciliation.

Why Bank Reconciliation Statement important?

These are the main reason that tells the importance of a bank reconciliation statement:

- Prevent Errors and Accounting Inaccuracies: Manual data entry, duplicate entries, and missed transactions can cause issues. Here, reconciliation helps find the errors and prevent report or tax issues.

- Prevents fraud and theft: Comparing companies' records with the bank’s statement. It helps detect unauthorized transactions, missing deposits, or other fraudulent activities. It helps prevent theft and protects financial assets.

- Enhance Financial Control: Regular reconciliation gives control over finances. It confirms that no transactions are overlooked. The cash balance matches accurately. It helps manage funds and avoids overdrafts or penalties.

- Support Reliable Reporting: Accurate and reconciled records are important for financial reporting.

- Helps in Audit and Tax Preparation: A bank reconciliation statement provides a clear and accurate audit trail. It makes the audit process easy and ensures that tax returns are accurate.

- Errors (Bank or Book Errors): Errors may come in the bank records or the business books. It includes: double entries, incorrect amounts recorded, transposition errors, and bank posting mistakes.

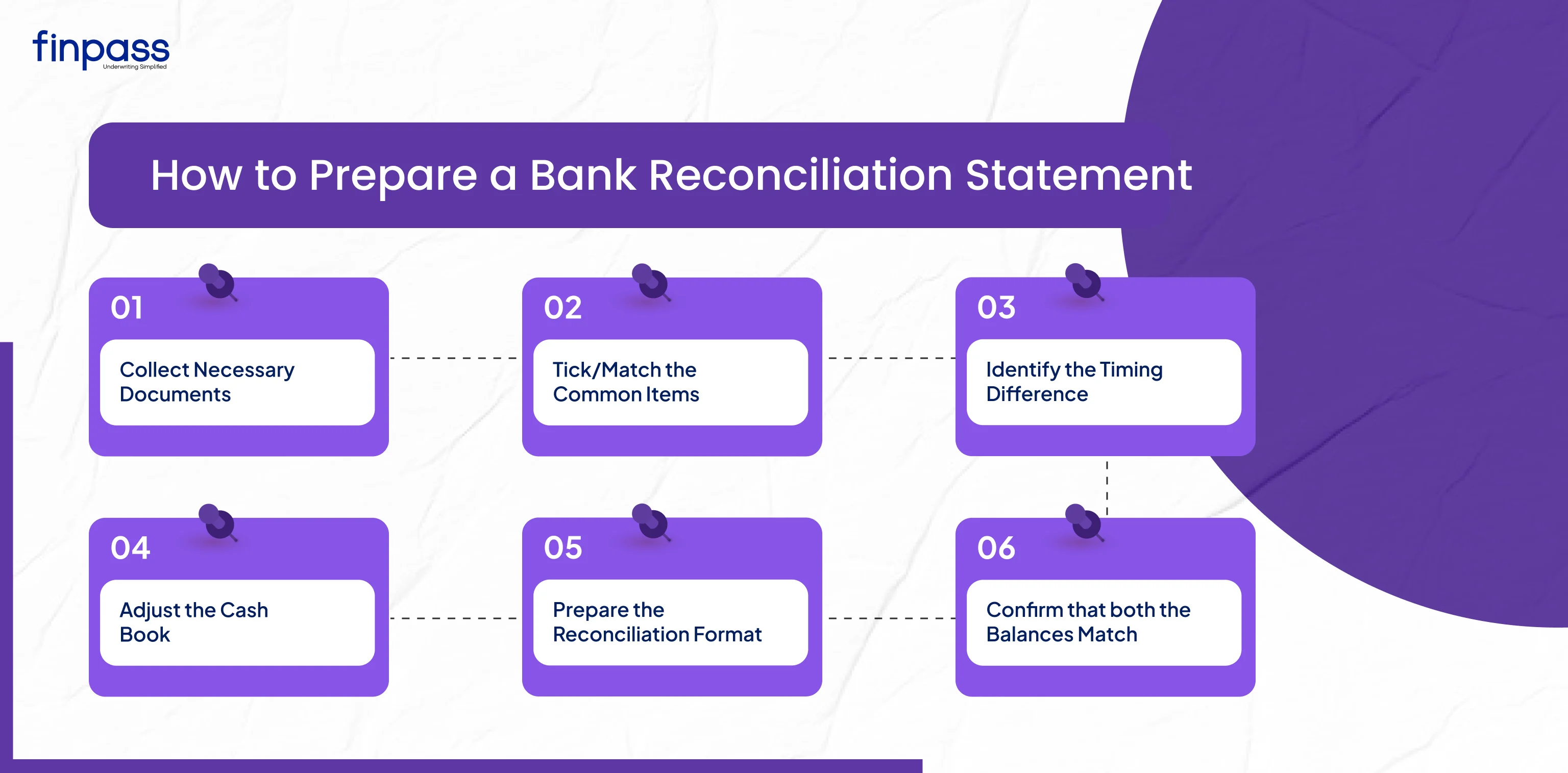

How to Prepare a Bank Reconciliation Statement: Step-By-Step

Here is a simple step-by-step overview of a bank reconciliation statement:

Step 1: Collect Necessary Documents

Collect bank statements and internal cash records for the same period. Any supporting documents, as deposit slips, receipts, and voided check records.

Step 2: Tick/Match the Common Items

Compare the cash book and bank statement line by line. Tick all the transactions that appear in both (e.g., deposit, cheques cleared, withdrawals). After the unmatched records are entered into the BRS.

Step 3: Identify the Timing Difference

Timing differences occur when a transaction is recorded in one book but not in the other. Check these things:

- Outstanding Checks

- Deposit in Transit

- Bank Credited Amounts Not in Books

- Bank Debited Amounts Not Recorded in Books

Step 4: Adjust the Cash Book

Update the Cash Book for all transactions that the bank has recorded but not in your records. You need to make adjustments for:

- Bank Charges and Penalties.

- Interest Credited.

- Direct Debits.

- Errors in the Cash Book.

Step 5: Prepare the Reconciliation Format

Prepare the actual Bank Reconciliation Statement: the two common types are:

A. Starting with Bank Statement Balance: Add items that increase the bank balance and subtract items that reduce the bank balance (like outstanding checks).

B. Starting with Cash Book Balance

- Add bank credits.

- Subtract bank debits.

- Adjust for timing differences and errors.

Step 6: Confirm that both the Balances Match

At the end, your main duty is to adjust the bank balance to the cash book balance. They should be equal and matched.

Common Mistakes in Bank Reconciliation and How to Avoid Them

These are the common mistakes a business makes:

- Inconsistent Reconciliation

Many businesses reconcile only at the month's end. It allows discrepancies to pile up at the last. To avoid this, businesses should do reconciliation daily, weekly, and monthly basis.

- Ignoring Small Mismatches

Small entries are often ignored, which can lead to errors such as missing entries, double entries, and fraud patterns. You can avoid it by investing in every mismatch, marking recurring discrepancies for pattern analysis.

- Missing Bank Fees

Charges like ATM fees, SMS Charges, service charges, penalties, and auto-debits are often not updated in the cash book.

- Misreading or Misrecording Transaction Dates

Recording transactions under the wrong date or period creates timing mismatches. Deposits in transit and outstanding checks become difficult to track. Follow the value date from the bank statement. Review end-of-the-month postings carefully.

- Blind Trust on Software Outputs

Sometimes, businesses trust accounting software blindly or bank feeds blindly without verifying mismatches. Bank feed can fail and import errors can occur, and rules may miscategorize. That’s why a manual review is required.

Conclusion

As bank statement-related fraud is increasing, it's become extremely important for the business to conduct a bank reconciliation statement (BRS). In simple words, BRS means matching the cash book records to the bank statements. It helps identify the differences, errors and fix them. You can easily conduct BRS in 5 simple steps that include collecting of cash book and bank statement, comparing records, finding the errors, fixing the errors, and matching records.

FAQs

Ques: What is a bank reconciliation statement?

Ans: It is a financial document used to compare and reconcile a company's internal cash book balance with the bank statement.

Ques: What are the 4 steps of bank reconciliation?

Ans: The 4 steps of bank reconciliation are:

- Compare Records.

- Detect mismatches and errors.

- Make adjustments.

- Reconcile the balances.

Ques: What are three methods of bank reconciliation?

Ans: The three methods of bank reconciliation include:

- Adjusted Balance Method

- Balance Sheet Method

- Bank Statement Method

Ques: What is the formula for bank reconciliation?

Ans: The bank reconciliation includes two formulas:

Bank side formula

Adjusted Bank Balance = Bank Statement Balance + Deposits in Transit - Outstanding Checks ± Bank Errors

Book side formula

Adjusted Book Balance = Cash Book Balance ± Unrecorded Transactions ± Book Errors

Ques: What is the main objective of bank reconciliation?

Ans: Its main objective is to confirm that the company's cash book balance matches the bank statement balance.