-2.webp)

Comparative Balance Sheet helps in analysing financial statements. It helps in comparing the reports of 2 or more financial years or for any given period. Businesses can compare financial statements and find trends. Here in this blog, you will learn about the Comparative Balance Sheet.

What is a Comparative Balance Sheet?

A Comparative Balance Sheet is a side-by-side comparison of the full balance sheet report of a current accounting period and the previous accounting period. Comparison helps in identifying trends, direction of change, analyzing, and taking the right action. It provides a comparison of a company’s assets, liabilities, and shareholders' equity.

Components of a Comparative Balance Sheet

These are the essential components of the Comparative Balance Sheet under the comparative statement:

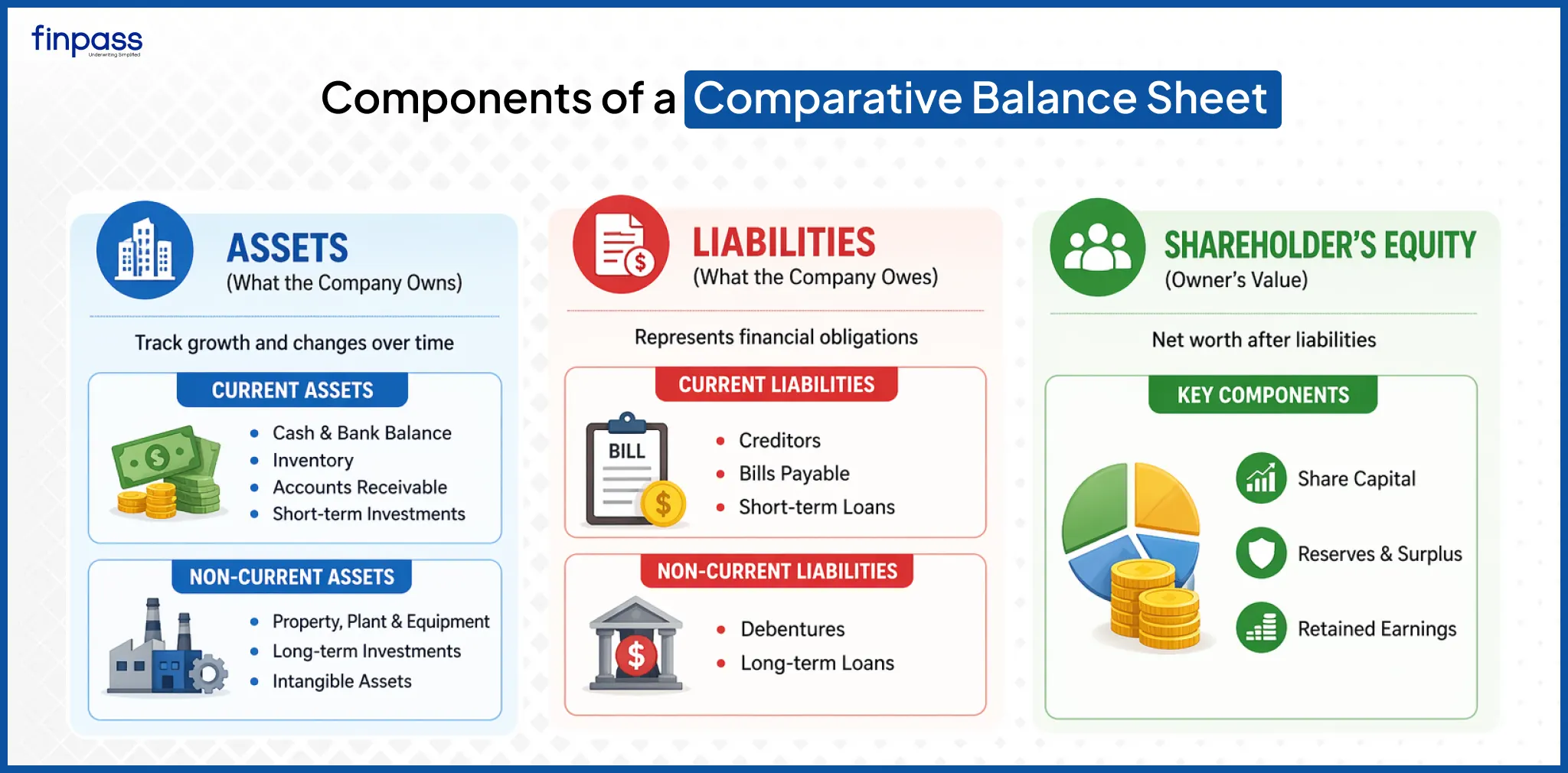

Assets

Assets represent everything the company owns. In a comparative balance sheet, assets are shown for multiple periods to analyze increases or decreases.

- Current Assets: Cash, bank balance, inventory, accounts receivable, and short-term investments.

- Non-Current Assets: Property, plant, equipment, long-term investments, intangible assets.

Liabilities

Liabilities represent what the company owes to others:

- Current Liabilities: Short-term obligations such as creditors, bills payable, and short-term loans.

- Non-Current Liabilities: Long-term debts such as debentures, long-term loans.

Shareholder’s Equity

It reflects the owner’s claim on the business after liabilities are deducted.

- Share Capital

- Reserves and surplus

- Retained earnings

Purpose of Comparative Balance Sheet

These are the reasons why a comparative balance sheet is prepared:

- It helps to analyze financial position changes over different periods.

- Identifies an increase or decrease in assets, liabilities, and equity.

- It helps in understanding the growth trends of a business.

- Helps investors and stakeholders in checking financial stability.

Comparative Balance Sheet Sample

Comparative Balance Sheet as on 31st March 2024 and 31st March 2025:

Particulars | 2024 (₹) | 2025 (₹) | Absolute Change (₹) | % Change |

Equity and Liabilities | ||||

Share Capital | 5,00,000 | 6,00,000 | +1,00,000 | 20% |

Reserves and Surplus | 2,00,000 | 2,80,000 | +80,000 | 40% |

Long Term Borrowings | 3,00,000 | 2,50,000 | -50,000 | -16.67% |

Short-term Liabilities | 1,50,000 | 1,80,000 | +30,000 | 20% |

Total Liabilities | 11,50,000 | 13,10,000 | +1,60,000 | 13.91% |

Assets | ||||

Fixed Assets | 6,00,000 | 7,20,000 | +1,20,000 | 20% |

Inventory | 2,00,000 | 2,50,000 | +50,000 | 25% |

Trade Receivables | 1,50,000 | 1,80,000 | +30,000 | 20% |

Cash and Cash Equivalent | 2,00,000 | 1,60,000 | -40,000 | -20% |

Total Assets | 11,50,000 | 13,10,000 | +1,60,000 | 13.91% |

How to Prepare a Comparative Balance Sheet?

These are the steps involved in a comparative balance sheet:

- Collect Balance Sheets of Different Periods: Start collecting balance sheets for at least two accounting periods. They should be prepared using the same format for the right comparison.

- Arrange Data in a Column Format: A comparative balance sheet works better when data is placed side by side. This format allows you to instantly see the difference between years without scanning multiple documents.

Create a table with separate columns for:

Particulars (Assets and Liabilities)

Previous Year

Current Year

- List All Assets and Liabilities: Items must be grouped under standard headings such as Equity and Liabilities and Assets. Maintaining the same order for both years is important because it ensures consistency and avoids confusion while analyzing changes.

Equity and Liabilities (Share Capital, Reserves, Loans, and Liabilities). It ensures the sequence remains the same for both years.

Assets (Fixed Assets, Current Assets, etc.)

- Calculate Absolute Change: When both years are placed side by side. Your next step is to determine how much each item has increased or decreased. It gives a direct numerical difference and helps identify major shifts in financial position.

Absolute Change = Current Year - Previous Year

- Calculate Percentage Change: Absolute change doesn’t show the significance of the change. The change helps understand whether the increase or decrease is small or substantial in relation to the base year.

Percentage Change = Absolute Change / Previous Year ×100

- Verify Total for Accuracy: A balance sheet should always balance total assets and total liabilities.

- Interpret the Changes: The actual value of a comparative balance sheet lies in analysis. Preparing the numbers is not enough. You need to understand what those changes indicate the company's financial health, performance, and strategy.

- Increase in assets suggests expansion or investment

- Increase in liabilities - higher obligations

- Increase in reserves - profit retention

- Decrease in debt - improved stability

- Present in Final Statement: After completing calculations and verification, your next step is to present the statement in a clean and professional format.

- What to do: Prepare a table with:

- Two Years of Data.

- Absolute change column.

- Percentage change column.

- Proper headings and totals.

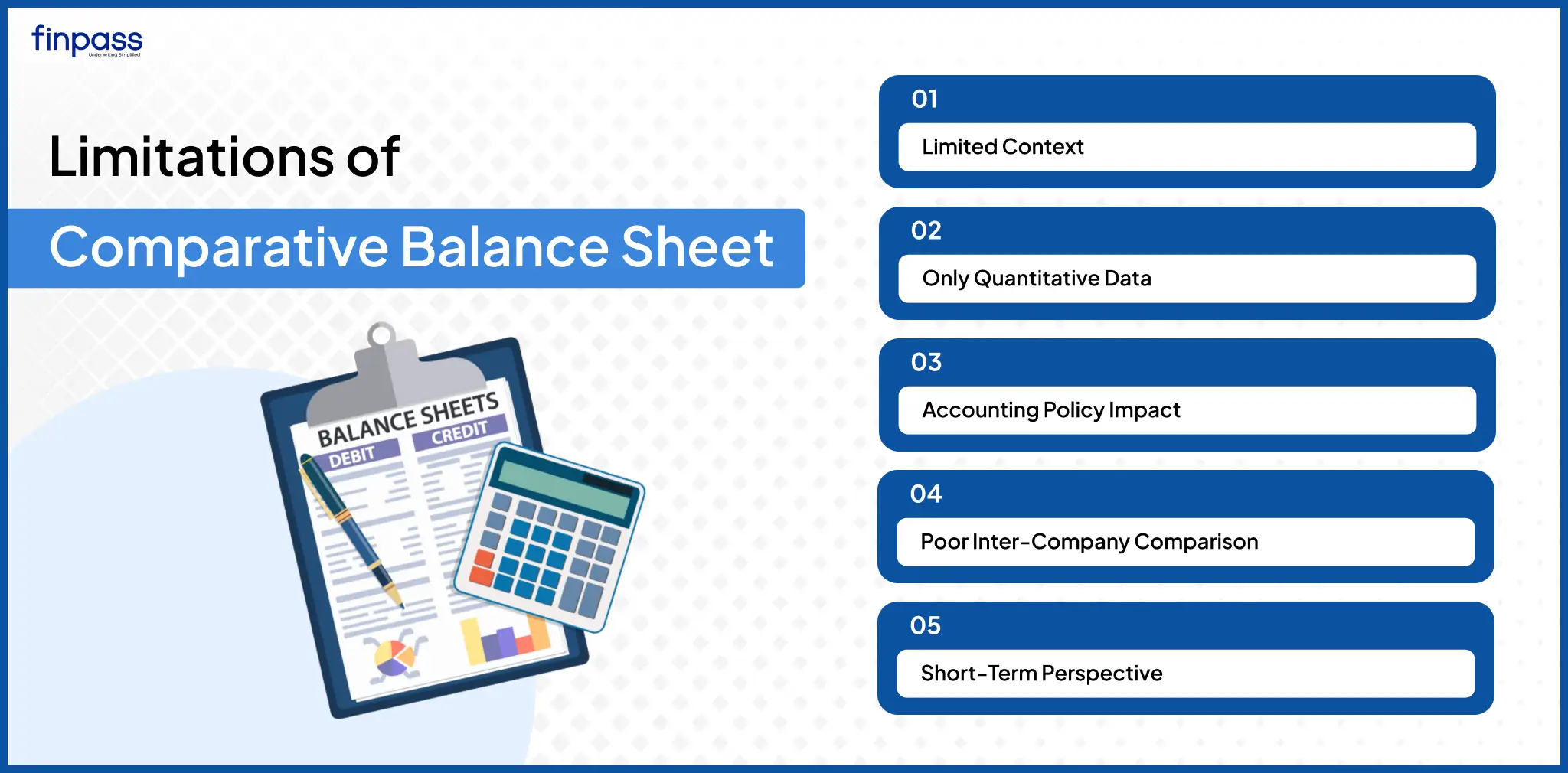

Limitations of Comparative Balance Sheets

It is an important tool in financial analysis, but it has certain limitations:

- Limited Context: It provides information about multiple accounting periods. However, it may offer a partial picture of the situation that influenced the changes in the financial position.

- Limited to Quantitative Analysis: The balance sheet only contains the numerical information. Important qualitative factors like management efficiency, market conditions, or brand value are not reflected. It can lead to incomplete analysis.

- Misleading Due to Accounting Policies: When a company changes its accounting methods (like depreciation or inventory valuation). Comparison between years can be misleading and may not reflect actual performance change.

- Not useful for Inter-Firm Comparison: Different companies may follow different accounting practices. It makes it difficult to compare the balance sheets.

- Short-term focus: It compares only two or a few periods, which may not be sufficient to identify long-term trends or patterns.

Conclusion

A Comparative Balance Sheet is an essential tool for assessing a company's financial health. The main components of the balance sheet are Assets, Liabilities, and shareholders’ equity. It offers several advantages and has some limitations.

FAQs

Ques: What is the Comparative Balance Sheet?

Ans: It is a side-by-side comparison of the balance sheet reports of different accounting periods.

Ques: Is a Comparative Balance Sheet useful for small businesses?

Ans: Yes, it is useful for businesses of all sizes. It helps track financial progress and areas needing improvement.

Ques: What are the common mistakes in preparing a Comparative Balance Sheet?

Ans: These are common mistakes you should avoid while preparing:

- Inconsistent Formats.

- Ignoring accounting policy changes.

- Calculation errors in percentage change.

- Not verifying totals.

Ques: What is the main objective of a Comparative Balance Sheet?

Ans: The main objective of the comparative balance sheet is to analyse changes in a company's financial position over time.

Ques: What is the absolute change in a Comparative Balance Sheet?

Ans: It is the difference between the current year and the previous year for each item.