Currently, financial institutions are seeing an increase in loan defaults and fake applications. It is difficult for the institution to segregate normal and risky borrowers. It increases the chance of financial loss. The credit risk analytics solve this issues. To know more about the reality of credit risk analytics until the end.

What is Credit Risk?

Credit risk is the possibility of non-payment of the loan by the borrower. It results in financial loss for the lenders.

For example:

- A bank gives a personal loan to a customer.

- Customer loses job and stops paying EMIs.

What is Credit Risk Analytics?

Credit Risk Analytics is the use of data analysis, statistical models, and machine learning techniques. It helps you evaluate whether the borrower defaults on the loan or fails to meet financial obligations.

It collects data (income, credit history, transactions, and alternative data). It applies to risk models, calculates risk scores, and supports lending decisions like approve, reject, or set interest rates.

It helps predict default probability, reduce default risk, automate lending decisions, offer risk-based pricing, and enhance portfolio performance.

Why Credit Risk Analytics is Important?

There are many reasons why financial institutions and lenders should focus on analytics for credit risk:

- Reduced Default Risk: Credit analytics helps in finding high-risk borrowers before making lending decisions.

- Enhance Decision Making: It uses data driven decision by checking many aspects instead of guessing.

- Enhances Profitability: It reduces the risk of losses and increases the over portfolio. This increases the profitability of lending firms.

- Speeds Up Loan Processing: The analytics tools add automation to the risk assessment process and speed up loan approvals.

- Detects Fraud Early: It helps in the identification of suspicious patterns and fraudulent applications.

- Helps in the right customer categorization: It evaluated and classifies customer segments according to their creditworthiness.

- Helps in early detection of Fraud: Analytics tools are designed to identify suspicious patterns and fraudulent applications early.

Main Components of Credit Risk Analytics

These are the main components of Credit Risk Analytics:

- Probability of Default (PD): It is a main financial metric that helps measure the default risk of a borrower. It helps in checking whether the borrower will pay or fail to pay the debt within a one-year timeframe.

- It calculates using factors like;

- Credit history and repayment behaviour.

- Income Stability and Employment Profile.

- Existing liabilities and credit utilization.

- Loss Given Default (LGD): It refers to the percentage of loss a lender can face if the borrower does not repay, even after recoveries (like Collateral or Repayments). It helps lending and financial institutions understand potential losses and helps in better risk mitigation. The loss given default depends on factors like:

- Type of Loan (Secured vs Unsecured)

- Collateral Value and liquidity

- Recovery process efficiency

- Exposure at Default (EAD): It is the total amount a lender is exposed to when a borrower defaults. It includes:

- Outstanding loan principal.

- Accured Interest.

- Any additional Credit Drawn.

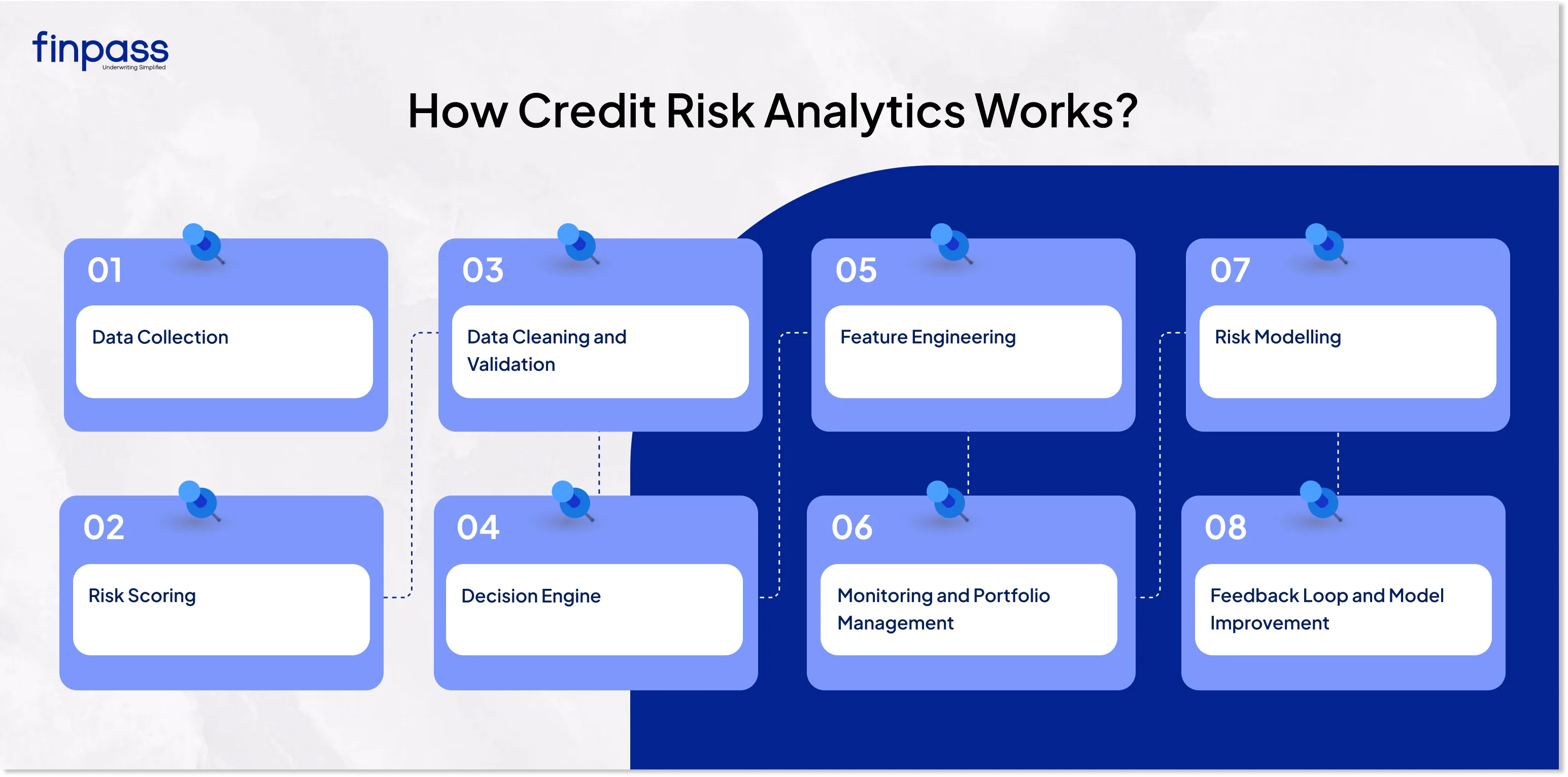

How Credit Risk Analytics Works?

A proper credit risk analytics process follows a sequence of events:

Step 1: Data Collection: Credit risk analysis begins with collecting borrower information from multiple sources to build a complete financial profile. This includes the collection of

- KYC data (PAN, Aadhaar, Identity Details).

- Financial Records (Income, bank statements, credit history).

- Transactional behaviour (spending and repayment patterns).

- Alternative data (GST, UPI, Telecom Activity).

Step 2: Data Cleaning and Validation: The raw data is inconsistent and can be incomplete. It must be clean and verified before analysis. This step is essential for the accurate prediction of risk. It includes

- Eliminating duplicates and errors.

- Make consistent data formats.

- Verify document authenticity.

- Detect fraudulent or suspicious inputs.

Step 3: Feature Engineering: Raw data is converted into meaningful features that indicate creditworthiness. It helps in understanding borrower behaviour:

- Credit Utilization Ratio.

- Debt-to-income (DTI) ratio.

- Repayment history trends.

- Account Activity Patterns.

Step 4: Risk Modelling: Advanced statistical and machine learning models are applied to assess the likelihood of default. These models identify patterns and predict borrower risk:

- Logistic regression.

- Decision trees and random forests.

- Machine learning /AI Models.

- Probability of Default (PD) estimation.

Step 5: Risk Scoring: After data collection, cleaning, feature engineering, and risk modelling, the output is converted into a simplified credit risk score. It makes it easier for

- lenders to make decisions quickly.

- It assigns a numerical score.

- Categorises borrowers.

- Standardize decision thresholds.

Step 6: Decision Engine: Automated systems use predefined rules and scores to make real-time lending decisions. It reduces manual effort and speeds up approvals.

- Approve (low-risk applicants).

- Reject (high-risk applicants).

- Conditional approval (adjust intezrest rate, limit, tenure).

Step 7: Monitoring and Portfolio Management

Risk assessment continues even after loan approval. Continuous monitoring helps detect early warning signs and manage overall portfolio health.

- Track repayment behaviour.

- Identify delinquencies early.

- Monitor portfolio risk exposure.

- Optimize collection strategy.

Step 8: Feedback Loop and Model Improvement

This system continuously learns from outcomes to enhance accuracy and performance over time.

- Analyze defaults vs successful payments.

- Retain models with new data.

- Improve prediction accuracy.

- Update risk rules and thresholds.

Techniques Used in Credit Risk Analytics

These are techniques used in Credit Risk Analytics:

Statistical Models (Logistics Regression)

Statistical models like logistic regression are used to predict the probability of default. They analyze historical borrower data and assign risk based on patterns. These models are simple, reliable, and easy to interpret.

Machine Learning Models

Machine learning models such as decision trees, random forests, and neural networks help identify complex patterns in large datasets. It enhances prediction accuracy and handles alternative data sources.

Credit Scorecards

Credit Scorecards give numerical scores to borrowers' attributes such as income, repayment, history, and credit utilization. It helps lenders quickly classify borrowers into risk categories and make fast approval decisions.

Predictive Analysis

Predictive Analysis uses historical data and trends to predict future borrower behavior. It helps lenders anticipate defaults, optimize lending strategies, and take predictive risk management actions.

Role of AI in Credit Risk Analytics

AI makes risk analysis faster, smarter, and more accurate. It helps in real time decisioning that helps in loan approvals or rejection, which can happen instantly instead of taking days. AI also uses alternative data like UPI transactions, GST records, and spending patterns to evaluate people with strong credit histories.

It uses advanced algorithms and provides better accuracy. It detects hidden risk patterns that traditional models often miss. They are more suitable for future prediction as they learn from the new data, defaults, and repayment behaviour.

Conclusion

Credit Risk Analytics is essential for modern financial institutions. Financial institutions can’t reduce the risk of defaults with traditional methods. With risk analytics, lenders can identify risk, predict defaults, and make better lending decisions. It reduces chances of financial loss and enhances efficiency, speeds up loan approvals, and enhances overall portfolio performance.

FAQs

Ques: What is Credit Risk Analysis?

Ans: It is a process of checking the borrower’s creditworthiness and risk of defaults.

Ques: What are the 5 components of credit risk analysis?

Ans: The 5 components of credit risk analysis are Character, Capacity, Capital, Collateral, and Conditions.

Ques: What are the 4 types of risks in credit risk analytics?

Ans: The 4 types of risks in Credit Risk Analytics are:

- Default Risk

- Concentration Risk

- Downgrade Risk

- Counterparty Risk

Ques: What is the difference between PD, LGD, and EAD?

Ans: The difference between are:

- PD (Probability of Default)

- LGD (Loss Given Default)

- EAD (Exposure at Default)

Ques: Can Credit Risk Analytics detect fraud?

Ans: Yes, it helps in the identification of unusual patterns, fake documents, and suspicious behaviour early.