Banks and financial institutions face the risk that some borrowers may not repay their loans on time. Loan defaults disrupt cash flow and increase NPAs. That makes it extremely essential for lending organisations to use methods to reduce credit risk. Credit Modelling helps lending institutions make the right decisions. Here in this blog, you will learn about the Credit risk modelling.

What is Credit Risk Modelling?

It is a process of using a statistical, mathematical, or machine learning-based model to quantify the likelihood that a borrower will default on a financial obligation. It helps financial institutions check the creditworthiness of borrowers and the chance of financial loss.

What is the importance of Credit Risk Modelling?

Credit risk modelling is essential for:

- It helps banks identify risky borrowers before giving loans.

- It reduces the chances of loan defaults and financial losses.

- Enhance decision-making for loan approvals.

- Proper analysis helps in setting proper interest rates based on risk.

- Supports better risk management and financial planning.

- Improves the overall financial stability of the business.

- It helps maintain healthy cash flow and profitability.

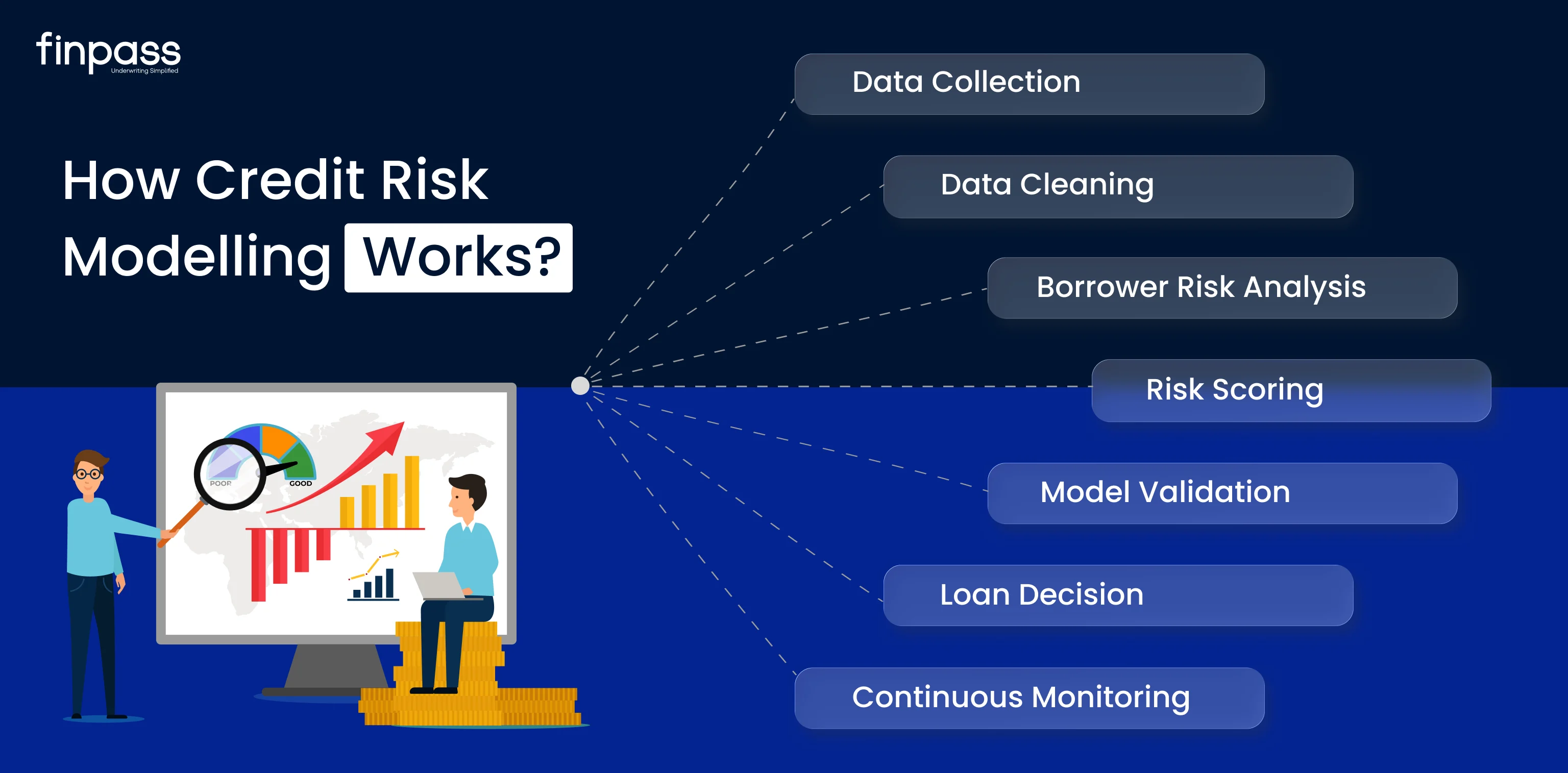

How Credit Risk Modelling Works?

This process involves several steps, including:

- Data Collection: The first step is data collection, where banks and financial institutions collect details such as income, employment status, credit history, existing loans, bank transactions, and repayment records.

- Data Cleaning: Collected data may contain missing values, duplicate records, or incorrect information. In this step, banks remove errors and organise the data into a proper format. Clean and accurate information helps the model give accurate results.

- Borrower Risk Analysis: After preparing the data, the model analyses the borrower’s financial condition and repayment behaviour. It examines factors such as income stability, debt level, payment history, and credit use.

- Risk Scoring: The system assigns a credit score or risk rating to the borrower. A higher score usually means lower risk; a low score means high risk. A score helps lenders in deciding loan eligibility, loan amount, and interest rates.

- Model Validation: Before a credit risk model is used in lending. The bank tests it using the past information. It helps check whether the model can accurately predict loan defaults and perform well under different market conditions. Validation helps improve model accuracy and reduce prediction errors.

- Loan Decision: According to the risk score and analysis results, the lender will decide whether to approve or reject the loan application.

- Continuous Monitoring: Credit Risk Modelling does not stop after loan approval. Banks continuously monitor borrower behaviour, repayment activity, and economic conditions. Models are updated regularly to ensure accurate assessment and better lending decisions.

What are the Key Components of Credit Risk Modelling?

The main components a business should know:

- Probability of Default (PD): It calculates the chance of a borrower failing to repay the loan.

- Loss Given Default (LGD): It calculates how much money a lender can lose if the borrower fails to repay the loan.

- Exposure at Default (EAD): It calculates the total amount exposed to risk at the time of default.

- Credit Scoring: It helps in evaluating a borrower’s creditworthiness through financial and credit risk information.

- Risk Rating: It classifies borrowers on the basis of credit risk level.

- Financial Data Analysis: Review income, debts, cash flow, and repayment capacity.

- Stress Testing: It shows that economic changes can affect the borrower’s ability to repay.

- Risk Management: It continuously tracks borrower performance and changes in credit.

Who should use Credit Risk Modelling?

Many organizations rely on it for making the right decisions, such as:

- Banks: Banks use Credit Risk Modelling to check whether a customer can repay a loan on time. It helps banks reduce bad loans and make safe lending decisions.

- NBFCs: Non-Banking Financial Companies use Credit Risk Modelling to assess borrower risk before approving personal loans, vehicle loans, or business loans.

- Fintech Companies: Fintech companies use credit risk models to determine credit limits, identify risky customers, and reduce payment defaults.

- Insurance Companies: Insurance companies use credit risk models to check the financial stability of policyholders and businesses before offering coverage.

What are the challenges a lending institution faces in Credit Risk Modelling?

These are challenges a lending institution faces during credit risk modelling:

- Poor Data Quality: Wrong, incomplete, or outdated data reduces the accuracy of the model and leads to incorrect credit decisions.

- Limited Credit History: There are many people who don’t have a past history. So, they may not perform well during economic crises, inflation, or sudden market changes.

- Fraud and Identity Theft: Fake documents, stolen identities, and fraudulent applications make risk evaluation difficult.

- Model Accuracy Issues: Credit risk models may produce incorrect predictions if assumptions or calculations are weak.

- Variations in Borrower Behaviours: You cannot rely on past spending and repayment behaviour of customers; it can change at any time.

- Cybersecurity Risks: Digital lending platforms face threats such as data breaches and cyberattacks. It can impact sensitive financial information.

- Difficulty in Predicting Defaults: Unexpected events such as a pandemic or economic crisis can increase loan defaults beyond model predictions.

Conclusion

Credit Risk Modelling is an important process that helps banks and financial institutions evaluate borrower risk and reduce financial losses. It uses customer information, financial analysis, and risk scoring methods to predict the chances of loan default.

FAQs

Ques: What is Credit Risk Modelling?

Ans: It is the process of using data and analytics to predict the probability of a loan default.

Ques: What is a Credit Risk Model?

Ans: It is a solution or system used by lenders to measure and manage the risk of borrower default.

Ques: What are the 5 C’s of credit risk analysis?

Ans: The 5 C’s of credit risk analysis are Character, Capacity, Capital, Collateral, and Conditions.

Ques: What is EAD vs PD vs LGD?

Ans: EAD is total exposure at default, PD is the probability of default, and LGD is the expected loss if default occurs.

Ques: What is the PD credit risk model?

Ans: It tells the probability of default on a loan within a specific time period.