Think you are a small business in India. You need a loan to buy before the festive season. But the bank asks for many documents and property as collateral. The whole process takes too much time. Here, OCEN comes and fixes this issue. In this blog, you will learn what the Open Credit Enablement Network is.

What is OCEN Full Form and Meaning?

OCEN full is the Open Credit Enablement Network. It is a digital framework in India that helps lenders, fintech companies, marketplaces, and other platforms provide loans digitally. In simple words, it acts like a common network that connects borrowers, lenders, loan service providers, and digital platforms. It allows businesses and individuals to access credit directly through apps or platforms.

What is the purpose of OCEN India?

It is launched to make loan approval easier and faster for people and small businesses. It helps MSMEs and underserved borrowers get access to formal credit. It creates a common digital framework for lenders and fintech companies. This eliminates paperwork and secure digital lending.

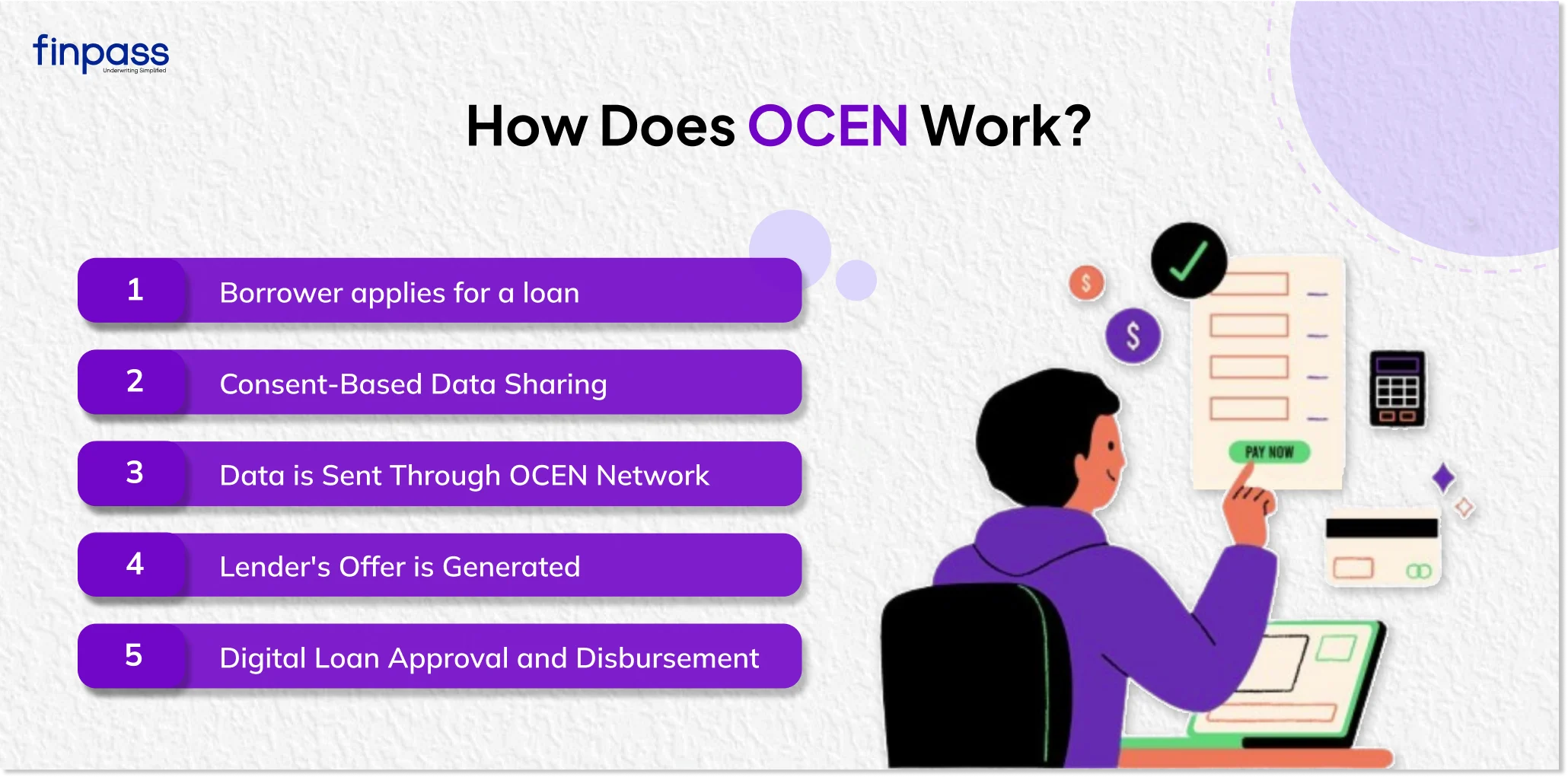

How does OCEN Work?

Here is how open enablement works:

- Borrower applies for a loan

A customer or small business applies for credit through a digital platform such as an e-commerce app, fintech app, or business marketplace.

- Consent-Based Data Sharing

Borrower permits to share financial data for analysis, like bank statements, GST data, transaction history, or business records, securely with lenders.

- Data is Sent Through OCEN Network

This framework provides a standardized framework that allows platforms, loan service providers (LSPs), and lenders to exchange data digitally and securely.

- Lender's Offer is Generated

Eligible borrowers receive customized loan offers with details such as loan amount, interest rate, tenure, and repayment terms.

- Digital Loan Approval and Disbursement

Once the borrower accepts the offer, the loan is approved digitally, and the amount is transferred directly to the borrower’s account.

Who Benefits from OCEN India?

There are many benefits of using this platform for MSMEs and borrowers:

- Easy Access to Credit: MSMEs, gig workers, and individuals can get loans digitally via marketplaces, accounting apps, e-commerce platforms, or fintech apps without visiting financial institutions physically.

- Faster Laon Processing: OCEN automates loan workflows using APIs, reducing paperwork and speeding up approvals and disbursals.

- Financial Inclusion: It is so helpful for the underserved businesses and people with limited credit history to access formal credit using alternate data like transaction history and cash flow patterns.

- Embedded Finance Opportunities: Platforms like e-commerce apps, GST software, or business apps can offer loans directly inside their ecosystem without becoming lenders themselves.

- Better Risk Assessment: Lenders can use consent-based digital information and behavioural insights instead of depending only on collateral or traditional credit scores.

OCEN vs Traditional Lending

Traditional Lending | OCEN-Based Lending |

Heavy Paperwork | Fully Digital Process |

Long approval timelines | Faster Approvals |

Physical Branch Visits | Online Applications |

Collateral Focused | Cashflow focused |

Limited Accessibility | Embedded Lending Anywhere |

Manual Verification | API based Automation |

Separate loan applications | Loans inside existing apps |

How OCEN Supports MSMEs?

MSMEs often face difficulties accessing formal loans due to a lack of collateral, limited credit history, and informal income structures. This platform helps MSMEs by providing digital credit access, eliminating documentation, speeding up approvals, and using alternative financial data for credit risk assessment.

OCEN and India Stack

It works with India’s digital systems like Aadhaar, UPI, DigiLocker, Account Aggregator, and eKYC to make digital lending faster and easier. These systems help lenders verify identity, access financial data with permission, check documents digitally, and transfer loan amounts securely.

India Stack provides the digital tools that OCEN uses to help both businesses and individuals get loans online with less paperwork and speed up loan approvals.

Examples of OCEN Use Cases

Here is how it is used to simplify lending:

- Seller Financing: E-commerce sellers can receive a working capital loan based on their sales history.

- Inventory Financing: Retailers can buy stock through embedded credit inside B2B apps.

- Gig Worker Loans: Drivers and delivery partners can access instant credit using their earnings information.

- MSME Working Capital Loans: Small businesses can obtain short-term financing through GST and banking information.

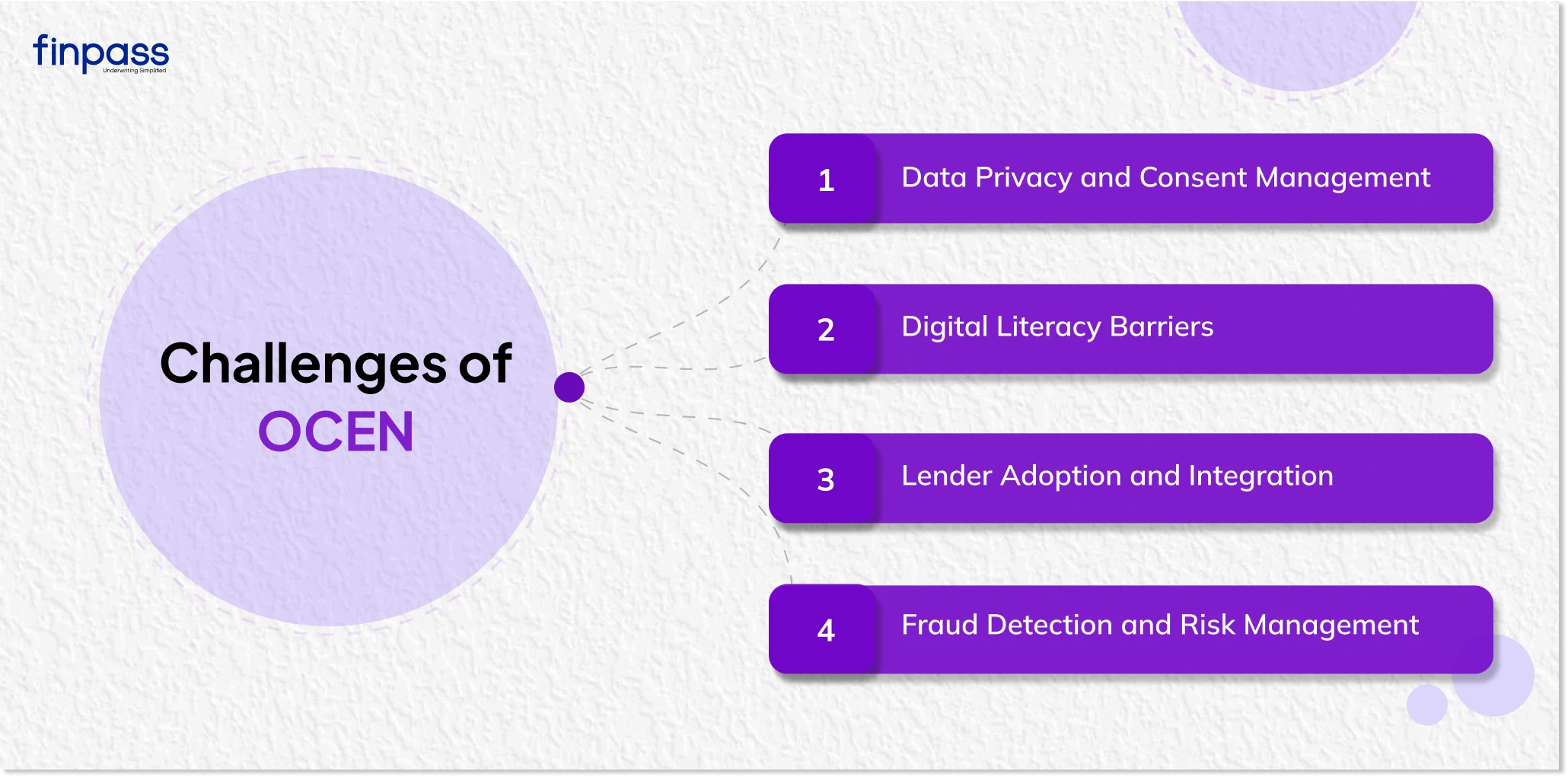

Challenges of OCEN

Several challenges need to be addressed for large-scale adoption:

- Data Privacy and Consent Management

OCEN relies heavily on consent-based data sharing. Borrowers share sensitive financial information such as bank statements, GST records, and transaction history online.

- Digital Literacy Barriers

Many small businesses and borrowers in rural or semi-urban areas are still not aware of digital lending platforms and a consent-driven financial system.

- Lender Adoption and Integration

Traditional banks and financial institutions often operate on their own systems. Integrating these systems with OCEN APIs and workflows may require significant technological upgrades, operational changes, and compliance adjustments.

- Fraud Detection and Risk Management

Fake documents, identity fraud, synthetic profiles, and misuse of online data can create lending risks.

Future of OCEN in India

It can change the lending system in India just like UPI changed online payments. It can make getting loans faster, easier, and completely digital for small businesses and individuals. More people and businesses use fintech apps and digital platforms. OCEN can help:

- Small businesses get loans easily

- Increase financial inclusion

- Reduce paperwork

- Credit services directly inside apps already use

Conclusion

OCEN is transforming how credit is distributed in India. It connects lenders, fintech companies, marketplaces, and borrowers via a standardized digital framework. OCEN allows faster, paperless, and more inclusive lending.

This platform opens the door for MSMEs, gig workers, and underserved borrowers to easy formal credit access.

FAQs

Ques: What is the full form of ONDC and OCEN?

Ans: ONDC stands for Open Network for Digital Commerce, while OCEN stands for Open Credit Enablement Network.

Ques: How does OCEN work?

Ans: It connects borrowers, lenders, and digital platforms via APIs to enable fast and paperless digital lending.

Ques: What is the OCEN Framework?

Ans: It is a standardized digital lending infrastructure that allows credit delivery across platforms and financial institutions.

Ques: Who developed OCEN India?

Ans: It is developed by the iSPIRT Foundation to enhance digital credit access and financial inclusion in India.

Ques: What is the main purpose of OCEN?

Ans: The main purpose of OCEN is to make credit access faster, easier, and more accessible for MSMSEs and underserved borrowers through digital lending.